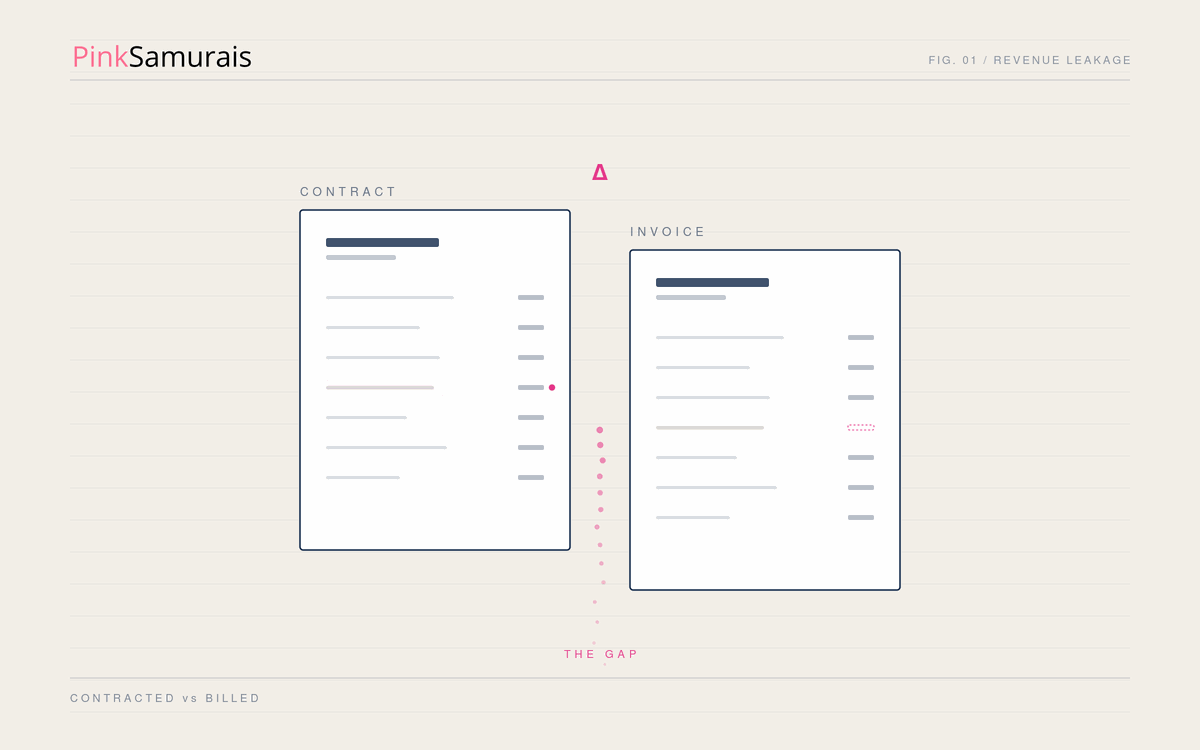

Most contracts say one thing. Most invoices say another.

The gap between the two is usually small enough to miss and large enough to matter. A pricing escalation that was never switched on. A discount that expired but keeps running. A contract amendment that never quite made it into the billing system. None of it trips an alarm. It just quietly drains margin, month after month.

This is revenue leakage, and for most software and subscription businesses it runs at 3 to 5% of revenue. This guide is a practical look at where it hides, why it stays invisible, and what finance and revenue operations teams are doing to close it.

Table of Contents

| Section | |

|---|---|

| 1) | The gap that costs 3 to 5% of revenue |

| 2) | Where the money actually leaks: the three usual suspects |

| 3) | Why leakage stays invisible |

| 4) | What finance and RevOps teams are doing about it |

| 5) | How to find your own number |

| 6) | Frequently Asked Questions |

1) The gap that costs 3 to 5% of revenue

MGI Research, the analyst firm that specialises in billing and monetisation, defines revenue leakage as the variance between contractually obligated revenue and actual recognised revenue. In plain terms: the money your contracts entitle you to, minus the money you actually invoice and collect. MGI puts that gap at at least 3 to 5% of revenue for the majority of companies, of every size. EY's widely cited estimate lands in the same band, at 1 to 5%.

Put a number on it. For a £30M ARR business, 3 to 5% is £900K to £1.5M leaving every year, without anyone noticing. For a £100M business, it is £3M to £5M. These are illustrative figures, not a measurement of your business, but the arithmetic is hard to ignore once you run it against your own revenue.

The important point, and the one most teams miss: this is not fraud, and it is usually not a pricing problem. It is a revenue capture problem. As MGI notes, leadership often responds to thin margins by raising prices, when the real issue is that revenue they have already earned is never being billed. You cannot fix a capture problem with a price increase.

2) Where the money actually leaks: the three usual suspects

In the billing and CPQ audits we run at PinkSamurais, three causes show up again and again, and rarely on their own. More often than not, an account has more than one running at the same time.

| The leak | How it happens | The tell |

|---|---|---|

| Pricing escalations never configured | A multi-year contract includes an annual uplift, but the increase is never set up in the billing system, so year two and three invoice at year-one rates. | Flat invoice amounts on contracts that should be stepping up |

| Expired discounts that keep running | An introductory or time-limited discount has an end date in the contract that was never implemented in billing, so it keeps applying long after it should have stopped. | Discounts still live past their contractual end date |

| Amendments that never reached billing | A tier upgrade, added users, or a renegotiated rate is agreed and signed, but the change never flows from the contract into the billing configuration. | Billed amounts that do not match the latest signed terms |

Pricing escalations that were never switched on

Annual uplifts are easy to agree and easy to forget. The clause sits in the contract, but unless someone configures the escalation in the billing system, the customer keeps paying the original rate. On a large multi-year deal, a single missed 5% uplift compounds quietly across the term.

Discounts that expired but keep running

Time-limited discounts are designed to end. In practice, the end date lives in the contract and not in the billing engine, so the discount keeps applying. This is one of the most common leaks we find, and one of the most recoverable, because the contractual basis to correct it is already in writing.

Amendments that never reached the billing system

Every mid-contract change is a handoff: from the people who negotiate it to the people who bill it. When that handoff is manual, things fall through. An upgrade gets signed but billed at the old tier. Added seats never appear on the invoice. The contract and the invoice drift apart, one amendment at a time.

3) Why leakage stays invisible

Leakage survives because nothing about it looks like a problem. The costs of delivery are incurred whether or not the revenue is captured, so the symptom shows up as a margin that looks slightly thin, not as a missing invoice. Teams diagnose a cost problem and miss the capture problem underneath.

There are signals, if you know where to look. MGI points to three financial tells: a rising Days Sales Outstanding (DSO) trend, contract assets or unbilled receivables growing faster than revenue, and deferred revenue that no longer reconciles cleanly to remaining contract obligations. Each is a quiet indicator that contracted and billed revenue have come apart.

There is also a compliance edge. MGI notes that once leakage exceeds the SEC materiality thresholds, around 5% of revenue or 10% of EBITDA, it stops being an operational nuisance and becomes an ASC 606 revenue recognition issue, with potential SOX 404 control implications for public companies. For a finance leader, that reframes leakage from a housekeeping task to a reporting risk.

4) What finance and RevOps teams are doing about it

The teams that close the gap treat it as a control, not a one-off clean-up. The common moves we see:

- Reconcile contract terms to billing configuration continuously, not once. The point of failure is the gap between what was signed and what is set up to bill. Checking it on a schedule catches drift before it compounds.

- Put alerts on the dates that leak. Escalation dates, discount end dates, and amendment events are all knowable in advance. Flagging them turns silent leaks into routine tasks.

- Run a periodic leakage audit. A focused review of a sample of accounts, comparing signed terms against the latest invoice, surfaces both the size of the problem and the specific accounts to fix first.

- Close the handoff between systems. The durable fix is a single source of truth across contract lifecycle management, CPQ, and billing, so an amendment updates billing by default rather than by memory.

None of this requires ripping out your systems. Most of the recovery comes from tightening the seams between the ones you already have.

5) How to find your own number

You do not need a platform project to size your exposure. A focused audit will get you a defensible estimate:

- Pull a representative sample of active contracts, weighted toward your largest and most complex accounts.

- For each, compare the current signed terms (rate, escalations, discounts, amendments) against the most recent invoice.

- Record every variance, and the annualised value of each.

- Extrapolate across the book to get a working estimate, then prioritise the accounts where the contractual basis to recover is clearest.

Most teams are surprised twice: first by how many accounts have at least one variance, and then by how much of it is straightforwardly recoverable because the contract already says so.

You can run that audit yourself, or we can run it with you. Our CPQ & Billing Health Check is a focused diagnostic that pinpoints where your contracts and invoices have drifted apart, and what it is costing you.

6) Frequently Asked Questions

What is revenue leakage?

It is the gap between the revenue your contracts entitle you to and the revenue you actually invoice and recognise. MGI Research defines it as the variance between contractually obligated revenue and actual recognised revenue.

How much revenue is typically leaking?

Analyst estimates put it at roughly 1 to 5% of revenue, with MGI Research estimating at least 3 to 5% for the majority of companies. For a £30M ARR business that is £900K to £1.5M a year.

Is this a fraud or a pricing problem?

Neither. It is a revenue capture problem: revenue you have already earned that never gets billed, usually because a contract term was never reflected in the billing system. Raising prices does not fix it.

How do we find out how much we are leaking?

Start with a focused audit of a sample of accounts, comparing signed terms against recent invoices, then extrapolate. It gives you both a defensible number and a prioritised list of accounts to correct.

Go deeper: the full picture

Revenue leakage is the highest-value piece of a wider challenge. For the complete view, covering the five challenges of fragmented operations, the billing scenarios you have to support, and what unified revenue operations looks like, read Revenue Operations Excellence: The Complete Guide to Quote-to-Cash Execution.

Sources

- MGI Research, Revenue Leakage Series (Parts 1 to 5), 2025: definition, scale (at least 3 to 5% of revenue), financial-statement impact, and ASC 606 materiality.

- EY revenue assurance estimates: revenue leakage of approximately 1 to 5% of revenue.